Q1 2026 Investment Market Update

Investment portfolios declined over the first quarter of 2026 as conflict in the Middle East impacted the performance of most asset classes, a sobering reminder of how quickly the investment landscape can shift. This broke a relatively consistent streak of portfolio performance from roughly 12 months ago, when the dominant conversation was tariff uncertainty rather than geopolitical conflict.

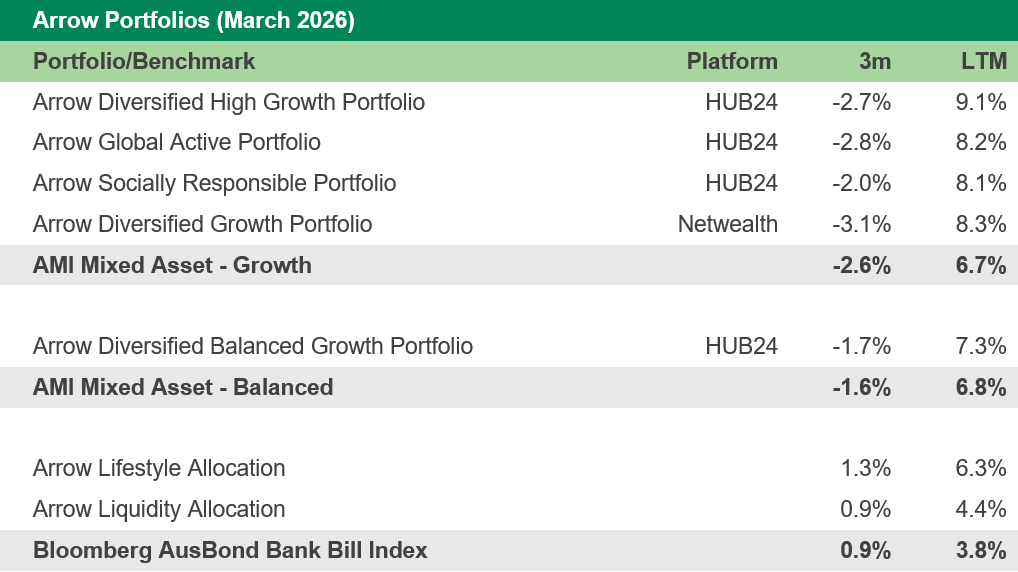

The volatility was largely contained to March, as hostilities escalated over the final weekend of February. Performance was positive across both January and February, but this wasn't enough to overcome a substantially negative March, the worst single month's performance since the COVID drawdown of early 2020. For the quarter as a whole, returns ranged between -3.1% and -1.7%, depending on the strategy.

Some of the numbers in this quarter's letter may feel larger than usual, and it would be remiss of me not to acknowledge the emotional considerations of investing during periods like this. When assessing performance in difficult markets, it is important to zoom out, month-to-month returns are inherently volatile, and sharp drawdowns can elicit emotional responses that are often counterproductive to sound long-term decision making. Long-term returns over the past 12 months, three years & longer horizons remain solid, and this should be where strategy and planning conversations are focused.

During the quarter, the Investment Committee made two portfolio adjustments, a new tactical allocation to value stocks within the global equity allocation and the purchase of Australian equities over the quarter's final weeks, increasing the level of risk at the portfolio level.

Whilst we did dip into our defensive reserves, portfolios ended the quarter continuing to hold a measured underweight to higher-risk assets, maintaining a deliberate tilt toward investments offering more stable and predictable total return profiles. This positioning reflects our disciplined and risk-aware approach, managing valuation risks in an environment of elevated asset prices and heightened geopolitical uncertainty.

Performance & Positioning

Portfolio performance continues to hold up favourably on both an absolute and relative basis, as shown below. Over the quarter, results were largely in line with peer groups, with some slight underperformance for certain portfolios, but over the last twelve months, the results remain solid, with a good level of outperformance across the board.

Leading into the period of market stress, our portfolios were defensively positioned, with allocations weighted toward defensive assets relative to growth. That said, some of the risk assets held within portfolios did experience drawdowns in excess of the broader market, a reflection of the significant dispersion in returns seen across equity markets during Q1. As noted in the Australian equities section later on, even within a single index, the gap between the best and worst performers was stark, and portfolios with any exposure to higher-growth or momentum-oriented equities were not immune to that volatility.

Importantly, the Investment Committee did not remain passive. During the quarter, deliberate changes were made at the portfolio level to better position clients for the recovery, increasing equity exposure and selectively adding risk. These adjustments were made to hedge upside risk in the event of a rapid V-shaped recovery, a pattern that has played out multiple times in recent years. Specifically, we allocated to higher-risk strategies well placed to benefit from any resolution or de-escalation in geopolitical tensions. These allocations were funded from the defensive component of portfolios.

Periods of drawdown are never easy, and the noise generated by financial markets and media during times of stress can make it tempting to act in ways that are not in the long-term interest of a portfolio. Our strong advice is to tune that noise out. We don't have a crystal ball, and we make no claim to being able to time markets with precision. Nobody can. What we can do is ensure portfolios are positioned to participate in the recovery when it comes, and that is exactly where our focus lies. For those clients considering deploying additional capital, it is worth noting that the valuation declines seen across asset classes during Q1 have meaningfully improved the long-term return outlook. In simple terms, you are buying the same assets at a lower price, which history tells us is a reliable foundation for strong future returns. The Investment Committee will continue to monitor conditions closely and act decisively where it is in our clients' best interests to do so.

International Equities

International equities declined 5.7% in Australian dollar terms over the quarter. Currency had a substantial impact, the Australian dollar rose 2.6% across the quarter overall, though it depreciated 4.1% in March alone as volatility spiked and safe-haven flows intensified.

We won't provide a commentary or prediction on the current Middle East crisis, however, we can translate the environment into portfolio construction implications. Geopolitical headlines drive fear, and under Trump's leadership the news cycle is incredibly unpredictable, markets swing repeatedly on tweets and Truth Social posts, making any near-term forecasting close to impossible. And even if you could accurately predict geopolitical moves, military strategy, and trade flows, translating that into actionable investment ideas and then anticipating the second and third order impacts on individual assets is a whole separate challenge.

What we can do, and do do, is read the lay of the land and navigate the hand we're dealt. Leading into this crisis, there were two largely recognisable dynamics at play. Firstly, asset prices and broad market valuations, particularly across Australia and the US, were elevated and trading at multiples well above historic averages. Secondly, the geopolitical environment had become increasingly volatile over recent years, with deglobalisation accelerating and flash points emerging globally. Taking both into consideration, we had positioned portfolios more conservatively, not because we were banking on any single catalyst, but because the environment was not particularly conducive to taking on risk. This was also occurring at a time when cash rates are the highest they've been in years, and rising, meaning multi-asset portfolios could generate decent all-in returns from more defensive assets. That positioning has aided performance over the quarter and will continue to do so should the situation escalate further.

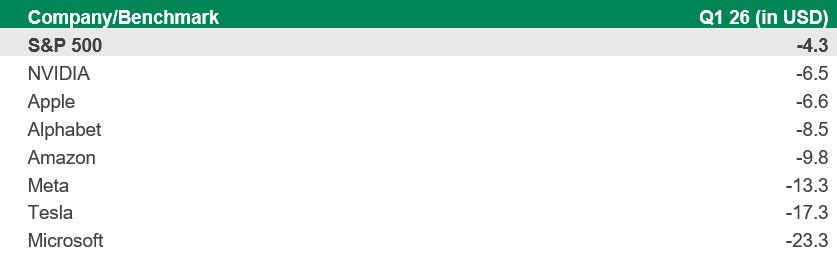

Turning to markets, every member of the Magnificent Seven delivered negative returns in Q1 2026, and every one underperformed the S&P 500's own decline of -4.3%. The spread of underperformance was notable, NVIDIA (-6.5%) and Apple (-6.6%) held up relatively better, while Microsoft (-23.3%), Tesla (-17.3%), and Meta (-13.3%) saw the steepest drawdowns. The common thread was a market reassessment of the AI capital expenditure cycle. Investors who had rewarded these companies for bold AI infrastructure commitments began demanding clearer returns on those outlays, with the hyperscalers facing particular scrutiny over spending plans that in some cases are projected to exceed operating cash flows. This was compounded by a broader rotation away from mega-cap growth into value, energy, and materials, alongside geopolitical risk from the Middle East conflict, adding to broader risk-off sentiment.

During the quarter, the Investment Committee made a change within the global equity allocation, electing to close out the UK equities position and redeploy the proceeds into a new value allocation. The UK position was established in mid-November 2024, at a time when valuation differentials between Australia and offshore markets were particularly attractive. Since its inclusion, the market materially outperformed Australian equities through 2025 and provided meaningful diversification, demonstrating negative correlation during periods of ASX weakness in late 2025, exactly what a diversifying allocation should do.

The proceeds were used to launch a new tactical position in value stocks. For the uninitiated, a value strategy places greater emphasis on the valuation of underlying securities relative to the broader benchmark, think Warren Buffett's Berkshire Hathaway. Our rationale is twofold. Firstly, by being more valuation-aware, a value strategy is naturally unlikely to hold the Mag 7 and high-multiple technology names, which means the portfolio is instead allocated across sectors and markets better positioned to capture a broadening of equity market returns. Secondly, while AI has been and remains the dominant investment narrative, much of the focus has been on the companies providing the capability, the picks and shovels, with less attention paid to the businesses well-positioned to adopt AI and convert it into improved efficiency and profitability. We believe value strategies are well placed to capture this dynamic, given the number of established, older-economy businesses poised to implement AI-led initiatives. We don't see this as a permanent allocation, it's tactical in nature, and we look forward to seeing how it unfolds over the coming couple of years.

Australian Equities

Australian equities declined -1.6% over the quarter, though our portfolio's Australian equity allocation underperformed the broader market due to greater exposure outside the index's largest names.

Whilst the headline number looks manageable, the drawdown was far from evenly distributed, and the average stock fell 5.5% against the index's return of -1.6%. This divergence was largely driven by the top companies in the benchmark outperforming the broader constituent base, meaning headline index performance masked the reality experienced by most investors. Technology and growth-oriented stocks were hit even harder, with selling commencing earlier in the year as innovation from Anthropic's Claude began challenging the software-as-a-service market and raising questions around business moats. This dynamic has been increasingly frustrating for fundamental investors, and the benchmark's largest constituents, Australian banks in particular, have remained difficult to own given their elevated valuations.

At the sector level, Energy and Utilities were the strongest performers over the quarter, returning 37.7% and 10.3% respectively, reflecting clear investor preference for sectors leveraged to the oil price and defensive income. Information Technology and Health Care were the weakest, falling 28.0% and 16.9% with the technology sell-off, as noted, having commenced before the outbreak of conflict.

One thing worth noting is that our local market and economy is arguably more susceptible to the second and third order impacts of the Middle East conflict than many appreciate, something that has become increasingly evident through fuel shortages in recent weeks. The Australian mining sector is the country's largest diesel consumer, using approximately 9.6 billion litres annually, representing roughly 35% of total national demand. Mining also makes up approximately 25% of the ASX, making it the second largest sector in the index. Whilst not all mining operations are domestically based, rising fuel prices are undoubtedly squeezing profitability, and the risk of fuel being diverted away from mining toward more critical industries is a real one. The latter is yet to fully play out, but the longer the conflict drags on and the Strait remains closed, the more that probability rises.

During the quarter, we made one change to the portfolio's Australian equity allocation, increasing equity exposure and selectively adding risk. We allocated to the Firetrail Australian Small Companies Fund and the Fidelity Future Leaders Fund, higher-risk strategies we expect would perform strongly in the event of a resolution or de-escalation in geopolitical tensions. We chose to express this view via the Australian equity allocation specifically, as it removes the need to take a currency position, and this part of the market had already been exposed to a meaningful sell-off in technology companies, an investment idea the committee had been separately considering for some time.

Property & Infrastructure

Property and infrastructure were among the better-performing asset classes across the portfolio over the quarter. Listed infrastructure delivered positive returns of 5.2%, while Australian listed property declined substantially (-16.6%), though this is not an asset class we explicitly allocate to. Our global listed real estate position appreciated 1.8% over the quarter, one of the best-performing assets within the portfolio.

The outperformance of listed infrastructure and global real estate over Q1 was underpinned by a confluence of factors that had been building well before the Middle East conflict escalated. Infrastructure, as an asset class, tends to demonstrate its value most clearly during periods of heightened uncertainty, offering resilient, contracted cash flows that are largely insulated from the economic cycle. The conflict has also brought inflation protection back to the forefront of investor thinking, with infrastructure & property assets, whose revenues are explicitly or implicitly linked to inflation, becoming increasingly attractive as fuel-driven price pressures have re-emerged and the risk of a more persistent inflationary environment has grown. Energy-aligned infrastructure has been a particular beneficiary, as accelerating power demand from data centres, rising electricity consumption driven by electrification and AI adoption, and the resurgence of geopolitical risk have all combined to sharpen investor focus on assets with genuine system-critical demand. The U.S. power market in particular has entered what many are describing as a power supercycle, with data centre demand alone expected to more than double by 2030. On the real estate side, improving property fundamentals across select global sectors, combined with stabilising funding conditions, have begun to restore confidence in the asset class after a difficult few years.

Direct real estate (being unlisted property assets) has had its best stretch in a while, particularly on a relative basis. The asset class has had a tough few years, coming out of the valuation resets triggered by the interest rate environment from 2022 onwards, it's pretty much been the one thing that hasn't worked across the 2022 to 2025 period. What we've noted more recently, however, is that many 12-month return figures are beginning to look quite favourable. Decent margins over cash, and the asset class has stayed the course whilst listed growth assets have broken down around it, providing portfolio resilience.

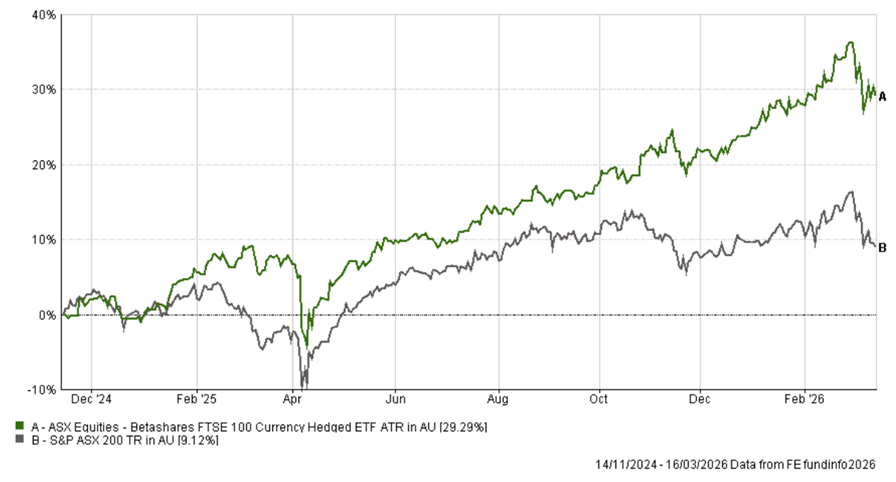

There was one small change within this allocation during the quarter, we trimmed our listed infrastructure position following a really strong stretch of performance. The allocation had returned 29.3% to the end of March, and in doing so had taken on a greater portfolio share than intended. The trim was a straightforward rebalance to lock in some of those gains and bring the weighting back in line.

Private Equity & Venture Capital

Private equity strategies delivered a quieter quarter. Core buyout strategies returned between -3.4% and +0.8% depending on the fund, while our venture strategy delivered -3.9%. It's worth noting we're still awaiting end-of-March valuations for a number of the underlying strategies, so these figures may be revised once received.

Whilst the absolute returns weren't great, the asset class did outperform the broader portfolio return across a declining market, which is the contribution you want from a diversifying allocation. It's also worth flagging that the asset class faced a currency headwind over the quarter, given that the majority of underlying assets are USD-denominated and the portfolios aren’t entirely hedged.

The standout news of the quarter was SpaceX filing confidentially for an IPO with the SEC on 1 April, targeting a June listing that would make it the first of what could be a trio of mega-IPOs, ahead of OpenAI and Anthropic. The offering is expected to raise up to $75 billion, more than three times the size of the largest U.S. IPO on record, at a target valuation of approximately $1.75 trillion. The news comes following SpaceX's February 2026 merger with Elon Musk's AI venture xAI. The financial engine underpinning that valuation is Starlink, which crossed 10 million subscribers globally and generated roughly $10 billion in revenue in 2025, with forecasts of $15–24 billion in 2026. For the broader VC market, the implications are significant. Early investors who participated in SpaceX's 2020 round at a $46 billion valuation are looking at massive paper gains. That kind of landmark outcome reinforces investor appetite for patient, long-duration bets on deep-tech and infrastructure plays, and signals a potential reopening of the IPO window for late-stage venture-backed companies after a prolonged drought. We hold exposure to SpaceX indirectly via a couple of different investments across the firm.

There were no changes to the private equity and venture capital allocation during the quarter.

Enhanced Income

Australian bonds delivered a return of -0.2% over the quarter, one of the better-performing asset classes across the period, though still underperforming cash.

The RBA delivered two consecutive rate increases in Q1 2026, reversing the easing cycle that had characterised much of 2025. In a unanimous decision on 3 February, the Board lifted the cash rate by 25 basis points to 3.85%, becoming the first major central bank to shift from rate cuts back to rate hikes following the post-COVID inflation episode. The rationale centred on a material pickup in inflationary pressures in the second half of 2025, with private demand growing faster than expected, capacity constraints tightening, and the labour market firming. A second hike followed on 17 March, a split 5-4 decision, taking the cash rate to 4.10%, with the Board flagging that Middle East conflict-driven fuel prices posed an additional upside risk to inflation.

Against that backdrop, defensive allocations spanning both Liquidity and Lifestyle strategies, which Arrow's advisers utilise broadly across the client base, delivered positive returns over the quarter, broadly in line with cash. Their floating rate structure proved particularly well-suited to the environment, with the two RBA rate hikes providing a direct tailwind to income generation. Importantly, these allocations meaningfully outperformed traditional fixed-rate bonds, which faced headwinds as yields rose in response to the RBA's tightening. This stands in contrast to the defensive sleeves commonly found in large multi-asset products such as those offered by Vanguard and BlackRock, where duration exposure detracted from returns. Clients holding Liquidity and Lifestyle allocations, therefore, benefited from both capital preservation and a meaningful buffer during the broader period of market stress.

Within the enhanced income component of our multi-asset portfolios, the Mutual High Yield Fund was a standout performer for the quarter, returning +1.3%. While modest in absolute terms, this outcome is meaningful in context, the fund has served as a deliberate ballast within portfolios, and its resilience during a period of broader market stress is exactly what it was designed to deliver. This is particularly noteworthy given that more traditional defensive exposures, such as bonds and duration-sensitive assets, declined over the same period.

During the quarter, the portfolio's exposure to defensive investments was reduced to fund the purchase of equities following the market correction seen across March, a deliberate and considered reallocation, the rationale for which is covered in the portfolio positioning section below.

As we write this letter, markets have staged a meaningful recovery through April, with the catalyst being a ceasefire announcement between the US and Iran on 7 April, triggering one of the strongest single-week rallies of the year. The S&P 500 gained strongly over the week ending 10 April, bringing its year-to-date return to essentially flat, a remarkable recovery from a trough that had the index down nearly 10% from its January peak. It is worth tempering some of the optimism, however. The ceasefire is a two-week cooling-off period, not a resolution, and the underlying tensions remain very much alive. We would warn that if the Strait of Hormuz remains closed for six to twelve months, a global recession becomes very difficult to avoid.

As always, we are deeply grateful for the trust and confidence you place in us, particularly during periods of market stress when that trust matters most. Should you have any questions about anything covered in this letter, please don't hesitate to get in touch. We're always happy to discuss in greater detail.

Kind Regards,

Ryan Synnot

Head of Investment Management

Arrow Private Wealth

Similar Insights

Latest Insights

General Advice Warning:

Any general advice in this email does not take account of your personal objectives, financial situation and needs, and because of that, you should, before acting on the advice, consider the appropriateness of the advice, having regard to your objectives, financial situation and needs.