Digital Estate Planning Essentials

When most people think about estate planning, they think about the obvious things: a Will, powers of attorney, superannuation nominations and perhaps a family trust structure. But modern life leaves behind more than paper files and bank accounts.

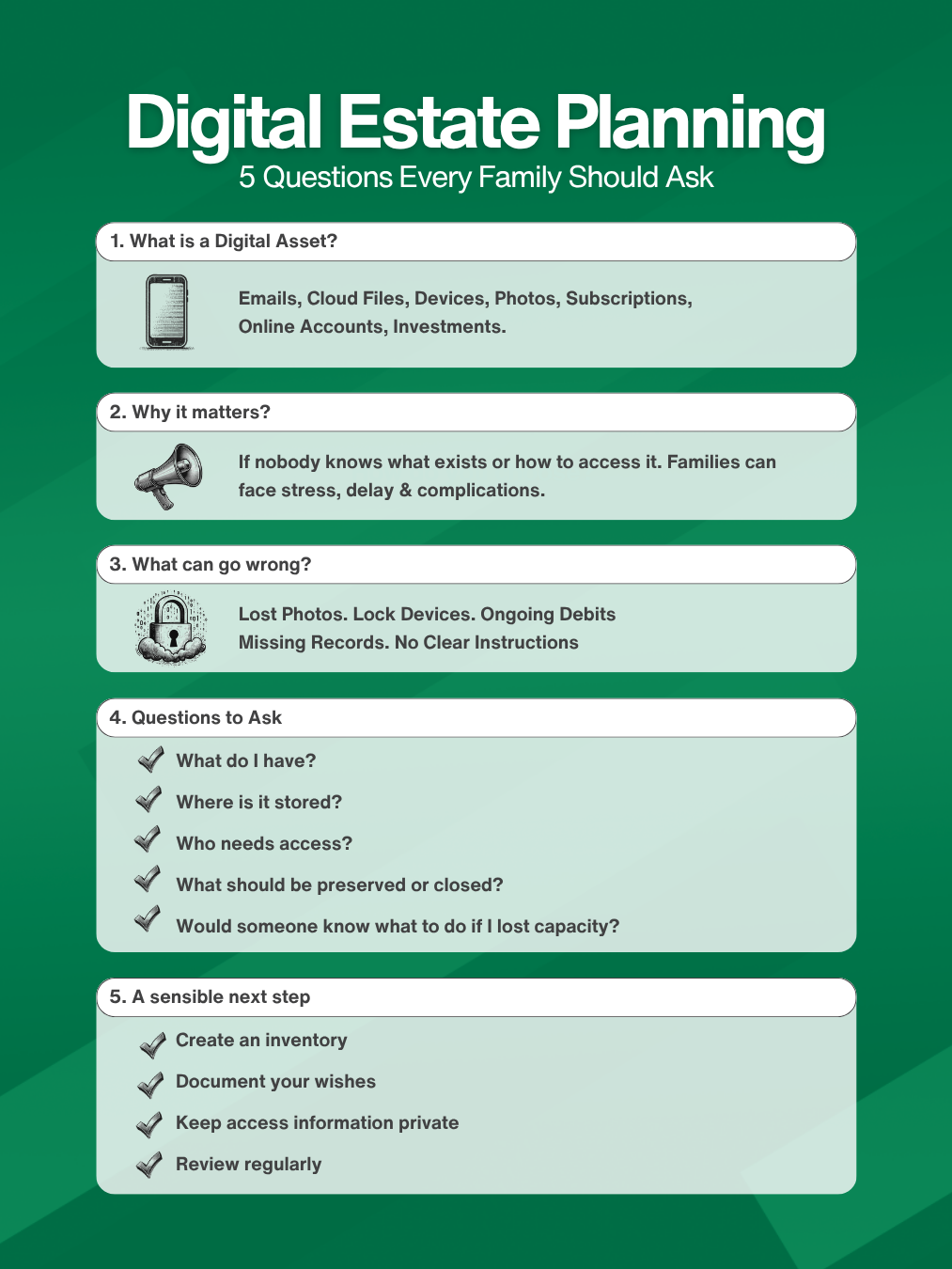

Today, much of our life is digital. Family photos may sit in the cloud. Bills may be paid automatically through online accounts. Important records may be stored behind passwords. Investment information, subscription services, social media profiles, email accounts, mobile devices and even loyalty programs can all form part of a modern estate.

That creates a practical problem. If something were to happen to you, would the right people know what exists, where it is, how to access it and what should happen next?

This is where digital estate planning becomes relevant.

Digital estate planning is not about chasing the latest app, gadget or cyber trend. It is simply about taking reasonable steps to organise the digital side of your life so that loved ones, executors and trusted advisers are not left dealing with confusion at the worst possible time.

Why this matters more than people realise

In many families, one person becomes the default organiser of digital life. They know the streaming subscriptions, the online banking logins, where the important files are saved, which phone contains the family photos and how the automatic payments are set up. Often, nobody else has the full picture.

That may not seem like a problem while everything is running normally. But death, illness or loss of capacity can expose how fragile that arrangement really is.

A surviving spouse may struggle to identify what accounts exist. Adult children may know there are family photos, but not how to retrieve them. An executor may discover online investment portals, recurring subscriptions or digital records, but have no clear roadmap. In business-owning families, the problem can be broader, with websites, domains, cloud files, software logins and shared systems all tied to one person’s knowledge.

The result is often delay, stress and unnecessary expense at a time when families are already under pressure.

The consequences can be practical, emotional and financial

The practical consequences are usually the first to show up. Accounts may be difficult to locate. Important records may be incomplete. Direct debits and subscriptions may continue unnoticed. Devices may be locked. Password resets may go to email accounts that nobody can access.

Then there is the emotional side. Some digital assets have no obvious dollar value, but enormous personal value. Family photos, videos, messages, documents and creative work can represent years of history. If they are lost, inaccessible or scattered across multiple platforms, that can create real distress for loved ones.

There can also be financial consequences. Digital assets may include online banking, investment platforms, cryptocurrency holdings, reward balances, business systems, digital invoices, tax records or documents needed for estate administration. Digital liabilities matter too. Automatic payments, renewals, domain registrations and software subscriptions can continue quietly in the background unless someone knows where to look.

In other words, digital estate planning is not just about technology. It is about continuity, visibility and reducing avoidable friction.

Questions worth asking yourself

A useful starting point is not a technical solution. It is a set of honest questions.

If something happened to you tomorrow, would someone know what digital accounts you have, which devices matter, where important documents are stored, how to locate key contacts, which subscriptions or automatic payments are running, and whether there are sentimental digital assets that should be preserved?

Would the right person know who should have access to what, and who should not?

Are your digital records spread across personal devices, cloud storage, email folders and paper files with no central logic?

Is there one person in the family who knows how everything works, while everyone else relies on them?

If you lost capacity rather than passing away, would your attorney or trusted family member be able to step in and manage what needs to be managed?

For many people, these questions quickly reveal the issue. The gap is usually not a lack of good intentions. It is that digital life accumulates gradually, while planning rarely keeps pace.

Some sensible principles to consider

The good news is that digital estate planning does not need to be overly complicated. In most cases, the objective is not to create a perfect system. It is to create a usable one.

First, build an inventory. Start by listing the categories of digital assets and accounts that matter. This might include email accounts, phones and computers, cloud storage, online banking, investment portals, superannuation access, social media, subscriptions, business systems, websites, digital photos and important records.

Second, distinguish between access and instructions. It is one thing for a trusted person to know that an account exists. It is another for them to know what you want done with it. Some accounts may need to be preserved, some closed, some transferred, and some simply reviewed.

Third, think carefully about who should have access. Not every person needs visibility over everything. Different people may need different levels of access depending on their role, whether that is spouse, child, executor, attorney or professional adviser.

Fourth, keep privacy in mind. The point is not to leave passwords lying around in an obvious place. It is to ensure that your system is organised, current and accessible to the right people in the right circumstances.

Fifth, review your arrangements over time. Technology changes, platforms change and families change. The digital footprint you have now is probably far larger than it was even a few years ago.

Importantly, detailed access instructions are generally better kept separately from the Will itself. A Will can become part of a public probate process, so practical digital instructions are often more appropriate as a separate document or appendix that can be updated more easily.

A planning issue, not a technology project

One of the reasons this topic gets ignored is that people assume it belongs in the “too hard” basket. It sounds technical, and many people understandably do not want to become unpaid IT managers for their own family.

That is why it helps to frame digital estate planning properly. This is not about becoming an expert in cyber security. It is not about finding the perfect software. And it is not about trying to predict every future technology.

It is a planning issue.

The aim is to reduce uncertainty for the people who may one day need to act on your behalf. For some families, the answer may be a simple, well-organised record of key accounts, assets and contacts. For others, it may involve a more structured approach to where important documents are stored and how access is managed. The right approach will vary, but the underlying principle is the same: clarity matters.

Final thoughts

Estate planning has always been about more than legal documents. At its best, it is about making a difficult time easier for the people you care about and improving the chances that your wishes can be carried out efficiently and appropriately.

Today, that means acknowledging that part of your estate may be invisible unless you deliberately bring it into view.

You do not need to solve every technical question to make progress. But it is worth asking whether your family could confidently deal with the digital side of your life if they had to.

For many people, that conversation alone is a valuable first step.

If you would like to explore the topic further, we discuss digital estate planning in more detail in our Arrow Insights video, which you can watch here.

General Advice Warning:

Any general advice on this page does not take account of your personal objectives, financial situation and needs, and because of that, you should, before acting on the advice, consider the appropriateness of the advice, having regard to your objectives, financial situation and needs. Information contained on this page was correct at the time of posting.